Cash is Dying, But Cards Are Still King—And Will Be for a Long Time

For years, futurists have been calling for the death of cash. The numbers now prove it.

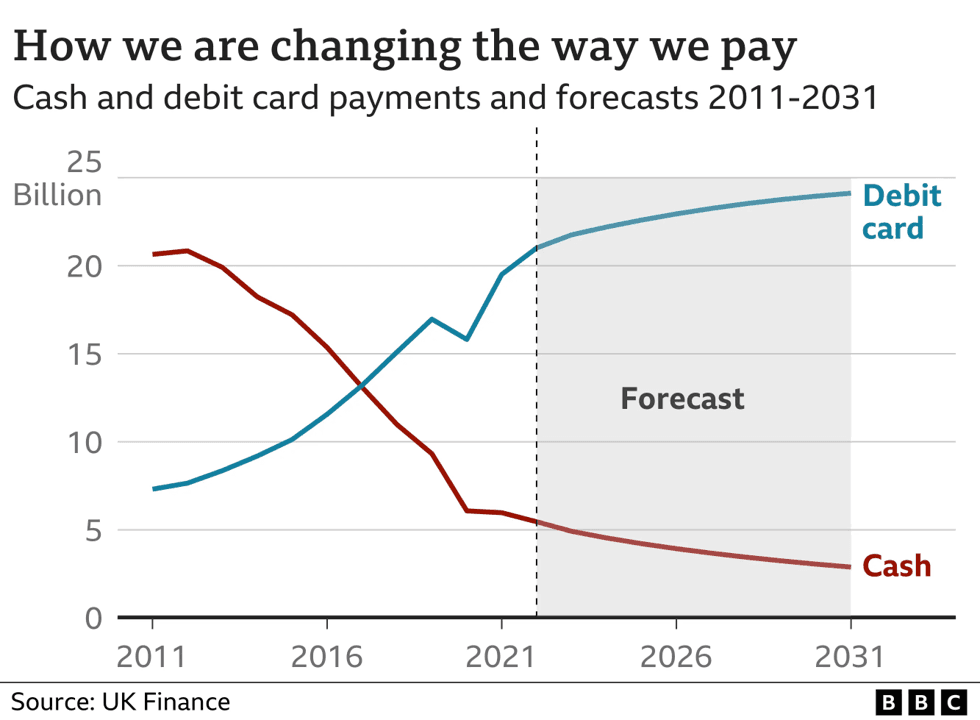

For years, futurists have been calling for the death of cash. The numbers now prove it: physical money is fading fast, with cash transactions in the UK dropping below 10 billion per year, down from over 20 billion in 2011. In the U.S., the Federal Reserve reports that credit and debit cards now account for over 60% of all payments, while cash use has collapsed to just 16% of transactions. Mobile wallets and alternative payments are growing, but the data makes one thing clear—credit and debit cards aren’t going anywhere. If anything, they’re growing.

A look at European e-commerce shows where the world is headed. While credit cards are expected to decline from 31% of e-commerce payments in 2023 to 15% in 2028, it’s not because of mobile wallets alone. Debit cards will continue to maintain a significant share of transactions, shifting slightly from 13% to 8%. Meanwhile, card-linked wallets—services like Apple Pay and Google Pay, which still rely on Visa and Mastercard networks—are set to increase from 24% to 30% over the same period. Even as mobile wallets rise, they are still tied to traditional card infrastructure.

In the U.S., the growth of debit card usage tells a different story. Unlike in Europe, where A2A payments and alternative fintech models are expanding, the U.S. is reinforcing its reliance on cards. Debit card transactions overtook cash payments years ago and are projected to keep climbing. By 2031, UK Finance projects that cash transactions will be nearly nonexistent in major economies, while debit and credit cards will continue their upward trajectory.

This isn't just an abstract trend—it’s already visible in consumer behavior. A 2024 Federal Reserve report found that even for transactions under $25, where cash was once dominant, credit and debit cards are now the preferred payment methods. The numbers reflect a clear consumer shift: people want the ease of tap-and-go payments, but they also trust the card networks that have been at the foundation of commerce for decades.

Despite the rise of mobile wallets, the vast majority of them are still backed by traditional credit and debit card networks. Apple Pay, Google Pay, Samsung Pay—these aren’t replacements for Visa and Mastercard. They are simply a different front-end experience for the same card-based infrastructure. While companies like Boku and alternative payment platforms claim that regional payment methods will dominate, the reality is that they are only adding more layers on top of the card networks, not replacing them.

The narrative that Visa and Mastercard are in decline simply doesn’t hold up under scrutiny. Even in markets where alternative payment methods are growing, card networks still facilitate the majority of transactions. The move away from physical cash has strengthened the position of digital card payments, and as more businesses phase out cash-only options, credit and debit card dominance will only grow.

What we’re seeing isn’t the end of cards—it’s the end of cash. If you’re placing bets on where payments are headed, don’t count out Visa and Mastercard just yet. The data shows they’re still the backbone of the modern economy, and they’re only getting stronger.

Follow Us

What Makes a Good Retail Center? How Midtown Crossing’s Co-Tenants Create Connected Shopping Trips

What Makes a Good Retail Center? How The Grove’s Tenant Mix Drives Cross-Shopping

World Cup Economic Impact on Retail: Which Businesses Benefited Most Near U.S. Stadiums?

Top 5 Best Location Intelligence Platforms for Retail Real Estate in 2026

Recent Blog Posts

Read the BlogWhat Makes a Good Retail Center? How Midtown Crossing’s Co-Tenants Create Connected Shopping Trips

10 min read

What Makes a Good Retail Center? How The Grove’s Tenant Mix Drives Cross-Shopping

10 min read

World Cup Economic Impact on Retail: Which Businesses Benefited Most Near U.S. Stadiums?

10 min read

Top 5 Best Location Intelligence Platforms for Retail Real Estate in 2026

5 min read